Estate Planning

Apr 23, 2026

Should a Family Member Be an Executor? Key Considerations and Alternatives

Family members are the people we trust the most, but are they a good fit to handle our estates when we pass?

A family trust can reduce taxes, protect assets, and transfer wealth across generations, but it comes with significant obligations. Here's everything you need to know.

Article Contents

A family trust is a legal arrangement created when a person transfers assets to a trustee, who manages them for the benefit of beneficiaries (often family members). In Canada, this legal structure has many tax and estate-planning benefits but is also governed by strict rules and regulations. Family trusts are a key estate planning tool because they allow families to create a lasting legacy while also protecting their assets.

That said, if you are planning an estate yourself — or acting as executor for an estate that involves a family trust — there are key considerations you need to be aware of. This guide will help you understand the creation, legal structure, mechanics, tax benefits, estate planning perks, costs and other rules surrounding family trusts in Canada. We’ll also look at what happens to a family trust when the settlor passes away: an important estate planning concept.

Whether you are in the beginning stages of planning your estate or you are a seasoned estate executor looking for some resources, this article will help you develop your understanding of family trusts in Canada.

A family trust is a legal arrangement where a settlor transfers assets—such as money, real estate, or investments—to a trustee, who manages them for the benefit of designated beneficiaries. This structure allows for asset protection, tax planning, and controlled wealth distribution, both during the settlor’s lifetime and after their passing.

The trust agreement outlines key details, including:

The trustee’s powers and responsibilities

The named beneficiaries (e.g., children, spouses, corporations)

How assets are managed and distributed

In Canada, trustees are often a parent, grandparent, or other trusted person and can also be a professional trustee." These are the people whose role and duty will be to manage the trust. The beneficiaries you can include in a family trust are children, spouses, grandchildren, parents, charitable organizations, or corporations.

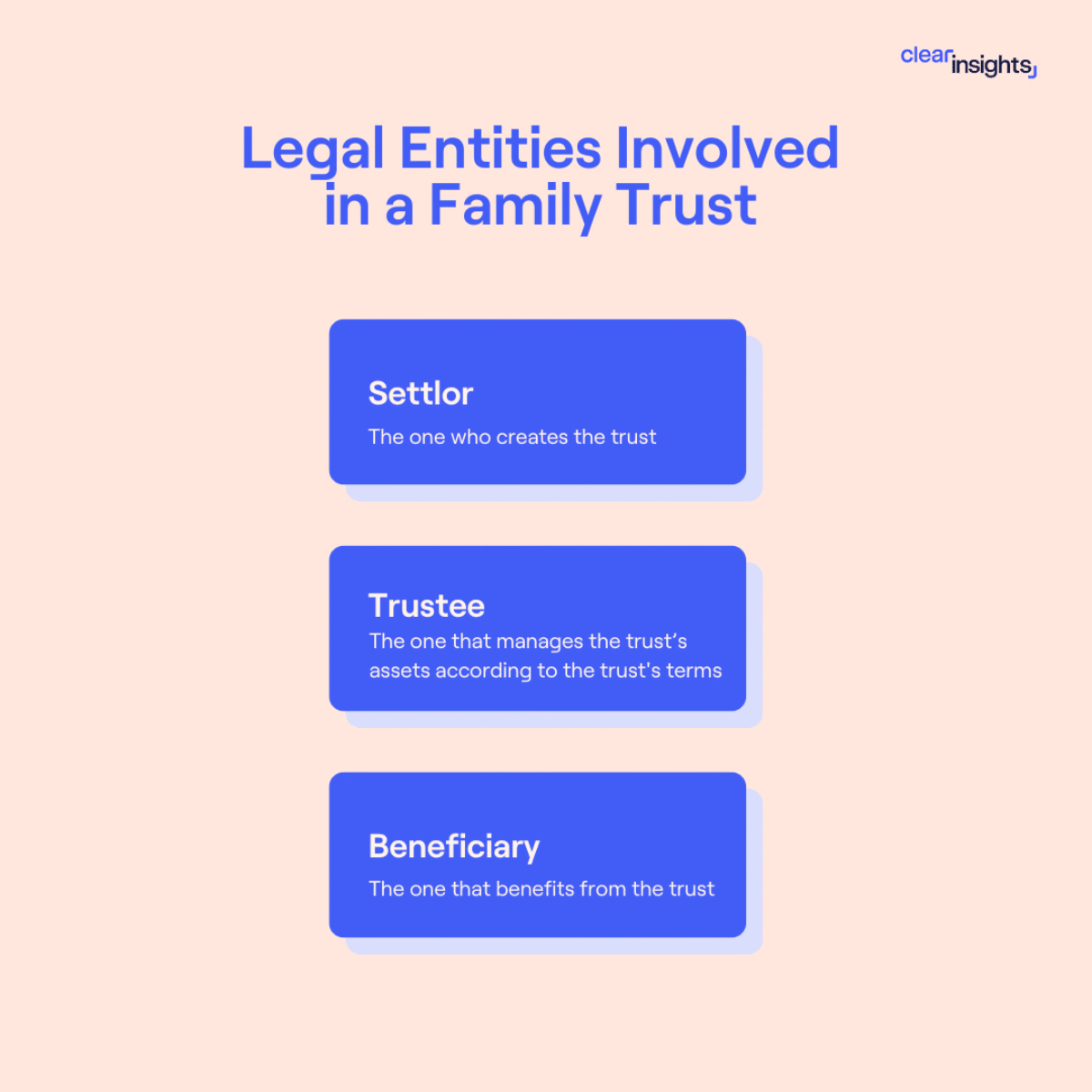

A family trust also involves three distinct roles:

The Settlor: The person who funds and establishes the trust. Once assets are transferred into the trust by the settlor, they are no longer their property.

The Trustee: This is the individual named to manage the assets and affairs of the trust. They hold and manage the assets of the trust for the benefits of the beneficiaries. Because of their role, a trustee is required to follow a number of duties such as: acting with prudence, acting in the beneficiaries’ best interests, to treating beneficiaries impartially, and to not personally profit from decisions made on behalf of the trust.

The Beneficiaries: These are the individuals, corporations, charities, trusts, etc., who will receive income or trust assets.

Remember: A trust is not a bank account. It is a legal relationship that separates the control of certain assets from the individuals benefiting from the assets. This separation is what creates both the tax advantages and the administrative obligations.

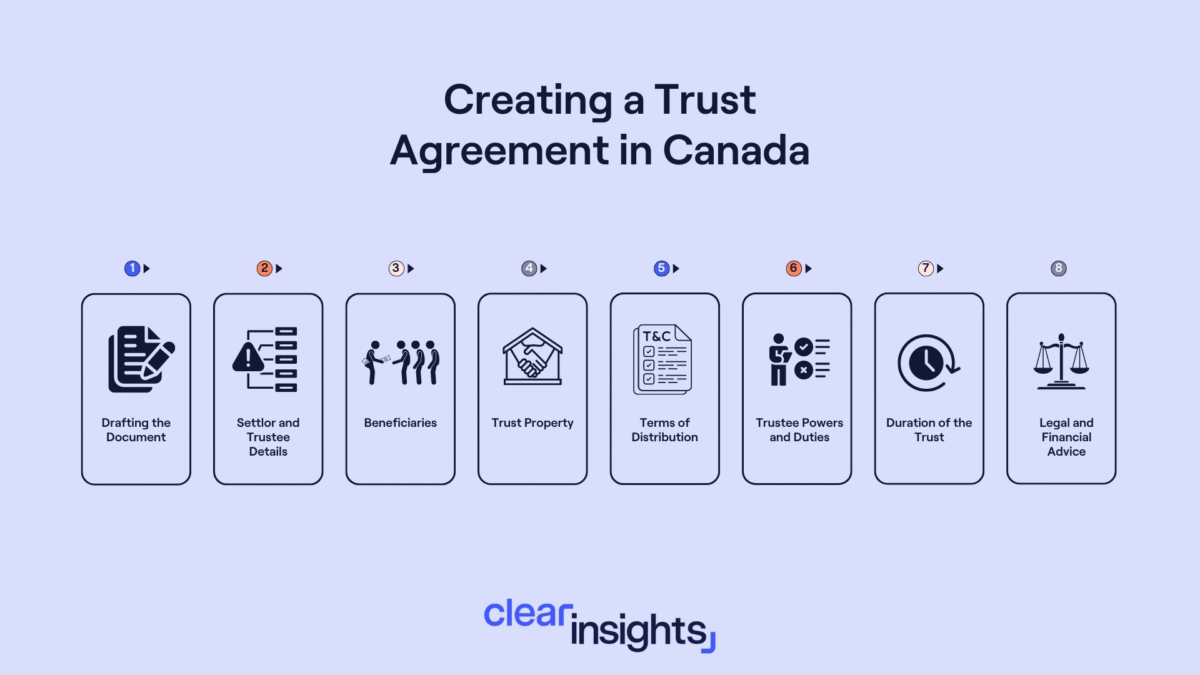

Creating a family trust in Canada in 2026 requires careful planning, legal compliance, and a clear understanding of your estate goals. Whether you're looking to protect your wealth, minimize taxes, or ensure a smooth transfer of assets, setting up a trust involves several key steps. Working with estate planning experts and legal professionals will help you structure the trust correctly and maximize its benefits.

Below is a step-by-step breakdown of the process to establish a legally valid family trust.

Define Your Objectives: Clearly determine the purpose of the trust, including how assets will be managed, protected, and distributed. Identifying your objectives ensures you choose the appropriate trust type—inter-vivos, testamentary, revocable, or irrevocable—to align with your financial and estate planning needs.

Select the Right Trustee and Beneficiaries: Choose a trustworthy trustee who will oversee the trust. Define their responsibilities and tasks in detail.,Clearly identify the beneficiaries and specify the assets they are to receive.

Draft the Trust Agreement with Legal Help: Collaborate with an estate planner and tax lawyer to draft a comprehensive trust agreement. This legal document should lay out the trust’s purpose, name the trustees and beneficiaries, and include clauses specific to asset management and distribution.

Fund the Trust: Make an initial contribution to the trust, which can be a nominal amount like a small sum of money or a symbolic item such as a silver coin.

Establish a Trust Bank Account: Open a bank account in the name of the trust to manage the trust’s finances effectively.

Asset Transfer: Transfer the designated assets into the trust. This may include a wide range of valuables such as real estate, vehicles, investments, and bank accounts. Be aware: transferring appreciated property to a typical family trust is treated by the CRA as a sale at fair market value. Any accrued capital gain becomes taxable in the year of transfer.

Finalize the Process: Implement a closing agenda with your tax practitioner to ensure all assets are transferred correctly and all legal formalities are completed.

On an annual basis, a T3 return usually must be filed with the CRA. The T3 return must be filed within 90 days of the trust’s year-end.

The cost to set up a family trust in Canada varies widely. The fees to draft the trust agreement could be anywhere from $1,500 to $10,000+ depending on the province you live in, the complexity of the trust.

Keep in mind that there may be additional costs aside from setting up the trust, such as legal fees to roll assets into the trust after it has been created. There are also ongoing costs as well. For example, most family trusts are required to file an annual T3 return, which is prepared by an accountant and costs up to a few thousand dollars.

By and large, trusts are an expensive planning mechanism and are only worth the cost and effort if you and your family receive large tax savings that outweigh the costs.

Choosing the right trustee requires assessing financial skills, reliability, and fairness. Beneficiaries should align with the trust’s purpose and be clearly designated.

The roles and responsibilities of trustees are to invest, manage, and distribute the trust’s assets. They must also perform administrative duties to ensure trust expenses and fees are paid. Beneficiaries may receive distributions of income and capital at the trustee's discretion, as set out in the trust deed.

Establishing a family trust is cost- and time-intensive, but these legal arrangements allow Canadian families access to a number of tax benefits that can outweigh legal and financial costs. Below are some of the most notable tax benefits of family trusts.

Since the development of the Tax on Split Income (TOSI) rules in 2018, income splitting (i.e. spreading income from higher tax bracket family members to lower tax bracket family members) has become much more difficult and complex to achieve. With the implementation of TOSI rules in the context of family trusts, dividends that are sent to family members through a trust are taxed at the highest marginal rate of the recipient — though exceptions exist.

That said, family trusts do allow for some income splitting so long as certain conditions are met.

One common structure that may allow for a TOSI exception is if family members are involved in the family business. From a structural perspective, a family business may set up a family trust with the children as beneficiaries, and have this trust own shares in their operating company. The company then issues dividends to the family trust, and these payments are allocated among the beneficiaries. From a tax perspective, if the beneficiaries receiving the dividend are actively engaged in the family business on a regular, continuous and substantial basis, their dividends may be excepted from TOSI rules.

There are other income splitting strategies but they fall outside the scope of this article. For more information on such strategies, we recommend consulting with a Chartered Professional Accountant or tax lawyer.

For families that own private businesses, family trusts allow for a key tax benefit: multiplying lifetime capital gains exemptions for family members.

If a family trust owns shares in a private corporation that are considered qualified small business corporation shares — or qualified farm or fishing property — and these shares are sold resulting in a capital gain, the beneficiaries of the family trust may be able to use their Lifetime Capital Gains Exemption (LCGE) to reduce their capital gains tax. With the LCGE limit at $1,275,000 for the 2026 tax year, this can result in significant tax savings if the exemption can be multiplied through multiple family members.

This is a complex concept so let’s look at a concrete example.

A Canadian family runs a small trucking business through a Canadian private corporation, ABC Corp. The corporation is owned by a family trust whose beneficiaries are the mother, father, and their two adult children. Assume the trust sells qualifying shares of ABC Corp to a third party, generating a $10,000,000 capital gain. With a 50% inclusion rate, the total taxable capital gain would be $5,000,000. If the trust allocates the gain equally among the four beneficiaries, each beneficiary realizes a $2,500,000 capital gain (or a $1,250,000 taxable capital gain). Each beneficiary may be able to use their own available LCGE, subject to the strict QSBC, trust, and personal eligibility rules. The family trust structure can substantially reduce the family's tax burden by multiplying access to the LCGE across multiple beneficiaries. However, it does not necessarily eliminate all tax on a $10,000,000 gain. Large LCGE claims can also trigger Alternative Minimum Tax (AMT), requiring careful planning.

Without a family trust in place, If only one parent owned the shares directly, only that individual's LCGE would generally be available, potentially resulting in significantly higher taxes.

Note: LCGE exemption benefits involving family trusts are very complex and require extensive tax planning for Canadians to meet eligibility requirements. Talk with a qualified professional if you have questions about using a family trust to reduce your capital gains tax.

Family trusts offer more than just tax benefits. They can also allow for asset protection and potentially reduce probate fees.

When you transfer your assets to a discretionary family trust, you protect them from lawsuits, creditors, and other unforeseeable claims. Since you transferred the asset to the trust, it does not belong to you or the beneficiaries. Once assets are placed in a discretionary family trust, they are shielded from many creditor and legal claims, especially when properly structured and not used to defeat existing creditors.

Although you may lose ownership of the assets after you create the trust agreement, you can maintain control by choosing a trustworthy trustee. It is generally not advisable for the settlor to act as the sole trustee because doing so can trigger attribution rules. Most planners recommend at least one independent trustee. You must also ensure you created a detailed trust document stating how everything should be done and the precise role of beneficiaries.

Crucial Tip: Control and protection of family assets can only happen if a trust is set up correctly. Under subsection 75(2) of the Income Tax Act, if someone contributes property to a family trust and the trust is structured incorrectly, the income and capital gains from that property can be attributed back to the settlor for tax purposes. This error typically occurs if the settlor is also named a beneficiary, and so the trust’s income and capital gains are taxed in their hands personally instead of in the trust’s. It’s important to remember that is why family trusts are initially settled with a nominal contribution (e.g. bills, silver coins) from someone who is not a beneficiary and does not contribute more to the trust. As a general rule, individuals who fund the trust should not be beneficiaries themselves. A poorly structured trust gives no tax benefits, but still comes with all the costs.

In terms of estate planning, family trusts offer a helpful benefit when dealing with probate. Depending on the province you live in, estates are typically subject to probate fees that are calculated based on the value of the estate. Family trusts can help Canadians avoid these fees as inter-vivos (i.e. living) trusts, which family trusts typically are, are not subject to probate. So, the value of any assets family trusts hold are not included in the value of the estate.

For example, let’s say an individual in Ontario passed away and their estate is valued at $500,000. Under Ontario’s Estate Administration Tax of ~1.5% of an estate’s value over $50,000, their estate would pay around $6,750 in probate tax. If the family member had a family trust created with them as trustee holding $250,000 of their total assets in trust, their estate would only pay $3,000 in probate tax instead.

Note: probate fees vary widely by province — they're negligible in Alberta and zero in Manitoba, so this benefit is strongest in Ontario, BC, and the Atlantic provinces.

In Canada, the 21-year rule in family trusts under the Income Tax Act contemplates that a family trust disposes of the property 21 years from the date it was created. This rule means that the trust’s assets are deemed disposed under subsection 104(4) of the Income Tax Act and a capital gains tax applies.

The main aim of this rule is to prevent indefinite deferral of capital gains tax on property held within a trust. The trust can continue after the 21-year mark, with subsequent deemed dispositions every 21 years thereafter.

This rule is very complex, so here is an example to help you understand its effects.

Assume a family trust was established in 2005 in Ontario, and the trustee held assets for the beneficiaries that were worth $500,000 at the time. Now in 2026, those assets are now worth $2 million. Roughly, the assets the trustee holds have accrued a capital gain of $1.5 million. They are now subject to capital gains tax on half the capital gains accrued, or $750,000. Under the CRA’s rules for family trusts, the trust would have to pay the top marginal rate (approximately 53.5% in Ontario). Assuming there were no tax credits or capital losses, the trust would owe around $401,000 in capital gains tax.

The tax consequences at the 21-year mark result in a major tax bill. What are families’ options when the 21-year anniversary of a family trust is looming? This is a very nuanced topic that requires consultation with an expert, but here are some basic strategies to be aware of.

Distributing the assets to beneficiaries before the 21-year mark to utilize a tax-deferred rollover, moving the future tax liability to the beneficiaries instead of triggering it within the trust. This rollover is generally only available where the receiving beneficiary is a Canadian resident. If beneficiaries live outside Canada the rollover does not apply and the trust will face the full deemed disposition.

Using the capital losses to cancel out the capital gains that may have been triggered by the disposition.

Strategically timing distributions to beneficiaries so the gain is realized in years when they have lower income.

Informing the beneficiaries of the potential capital gain tax liability and urging them to plan accordingly.

Note for Trustees: The 21-year clock starts from the date the trust is established, not the date of the first asset transfer. Trustees should track this date explicitly in their records and engage a tax expert at year 18 or 19 to plan the appropriate strategy.

From an estate administration perspective, it’s important to understand what happens with a family trust when the person who created it (the settlor) passes away. In this section, we will briefly outline what happens when a settlor of a family trust dies, starting with the least complex situation.

In cases where the deceased was only the settlor of a family trust and held no other role, the family trust continues, subject to any administrative or governance changes required under the trust deed. Family trusts in Canada are governed by the trustees, not the settlor, so the trust is not put in limbo.

If the settlor was one of multiple trustees, then nothing changes with the trust. The trustees continue to manage and handle the assets for the sake of the beneficiaries and annual T3 filings are still required.

While it is not common for the settlor and sole trustee of a family trust to be the same person, it does occur. In these cases when the settlor/trustee dies, then one of two things occur.

If the settlor named a successor trustee, then that person is appointed as the trustee of the family trust and continues to manage its assets.

If no successor trustee was named, then the beneficiaries or other interested parties can apply to the court to appoint a trustee in their place.

Note: Even if there is no acting trustee for a certain period, the family trust may still be required to file a T3 return.

If you are managing an estate and the deceased was a sole trustee, it can be extremely confusing to understand your role. Do you have a say in the trust? Do you need to determine what happens with the assets the deceased was managing?

In brief, no. In Canada, assets that are held in a family trust generally do not go through probate and are not the subject of the deceased’s personal estate if they were a trustee or settlor. As executor for the deceased, your responsibility is to manage the assets of the deceased pursuant to their will.

The only time there may be some overlap between your role as executor and a family trust managed by the deceased is if the deceased was owed anything personally from the trust (e.g. trustee compensation, trustee expenses reimbursements, etc.). These could count as assets of the deceased’s estate so you would be responsible for handling them accordingly.

Family trusts can be a major boon for the right families, but they are also very costly financially and administratively.. Before you set up a family trust in Canada, here are some costs and disadvantages of family trusts you need to be cognizant of.

High setup fees: Setting up a family trust can cost anywhere from $1,500 to $5,000 and up depending on the complexity of your family’s tax-planning structure. Note that this doesn’t include any other legal fees for rolling assets into a trust, for example. Setup costs can add up quickly.

Annual administration costs: Under Canada’s Enhanced Trust Reporting Rules, all family trusts in Canada — subject to limited exceptions — must file an annual T3 return and a Schedule 15 beneficial ownership disclosure. This is done regardless of if the trust earned income or made any distributions in the preceding year. The cost for having this done by a professional is anywhere from $1,000 to $3,000 and up depending on the complexity of the trust.

Administrative duties: Trustees of the family trust are required to document their work so they can properly account for the administration of the trust and their tasks completed. These records can be documented in various ways, but the administrative burden grows quickly.

Income-Splitting restrictions: Since the implementation of stronger TOSI rules in 2018, trying to use a family trust to income sprinkle or split income with family members is much more complicated.

The 21-year deemed disposition rule: For family trusts that plan to have a long lifespan, the 21-year deemed disposition rule can throw a wrench into their tax plans if not prepared for properly. And, preparing for it also adds planning and legal costs as well.

A family trust is a legal arrangement where a settlor transfers assets to a trustee to manage for beneficiaries (typically family members). They are used for tax planning, estate planning, asset protection, and intergenerational wealth transfers.

Family trusts structured correctly can allow for Canadians to avoid probate in some jurisdictions, multiply their lifetime capital gains exemption on business shares with other family members, and potentially protect assets from creditors in certain situations.

First, a trust deed is drafted by a lawyer, which sets out the terms of the trust. The settlor transfers assets to the trustee(s). The trustee(s) then manages those assets for the benefit of named beneficiaries. Income can be distributed to beneficiaries who report it on their own tax returns and the trust is required to file a T3 return each year.

At 21 years following the creation of a family trust, the CRA views the trust as having sold all its capital property at its fair market value, resulting in a major capital gains event. This rule is in place to prevent an indefinite capital gains deferral. It is crucial that trustees plan for this event well in advance.

In most cases, the family trust continues to be operated by the remaining trustees. If the deceased was the sole trustee of the trust, their successor trustee takes over. If no successor trustee was named, then an interested party (e.g. a beneficiary) may apply to the court to have one appointed. Note that the executor of the deceased has no say over the assets of the trust, but they may be involved in collecting amounts owed to the deceased trustee by the trust or facilitating trustee replacement.

Yes. Generally speaking, assets held in an inter vivos (e.g. family) trust are not subject to probate. As such, they are not subject to provincial probate fees, which can result in major cost savings.

The cost to set up a family trust in Canada varies, but it is around $1,500 to $5,000 and up depending on the complexity of the trust — not including moving any additional assets into the trust later on. There are also ongoing legal and accounting fees, such as filing a T3 return, which usually costs anywhere from $1,000 to $3,000 annually.

As an estate planning tool, a family trust secures your loved ones’ future and helps you minimize your tax liability, protect your assets, and avoid probate. Choosing a trustworthy and reliable trustee ensures you acquire superior asset management services before and after your demise.

Careful financial planning can help reduce the tax implications and allow you to enjoy the various tax benefits. As a settlor creates the trust, they must be aware of the 21-year rule in Canada and plan for it with the assistance of an estate planning expert. Book a free consultation with us, and let us help you safeguard your future.

The information provided in this article is for general informational purposes only and does not constitute legal, financial, accounting, or tax advice. It is intended to provide a high-level overview of Canadian estate planning concepts, including family trusts and related tax considerations, as they generally apply under the laws of Canada. Readers are strongly encouraged to seek advice from a qualified legal professional, accountant, or other licensed advisor before making any decisions regarding estate planning, taxation, or trust administration.

Secure Your Legacy

Secure Your Legacy

Get your free 12-step Estate Planning checklist now. 89% of readers complete their estate plan within 3 months of using our guide.

Instantly Access NowRelated articles

Estate Planning

Apr 23, 2026

Should a Family Member Be an Executor? Key Considerations and Alternatives

Family members are the people we trust the most, but are they a good fit to handle our estates when we pass?

Estate Planning

Mar 26, 2026

Bank Executor Services Versus Independent Executors: Understanding Your Executor Options

Want to work with a corporate executor but not sure where to start? ClearEstate compares professional executors from banks and other institutions.

Estate Planning

Feb 13, 2026

Executor of a Will: What the Role Involves and When to Seek Professional Help

Preparing an estate plan and feeling unsure about who to name as executor, or even what the role entails? We explain below.